Account Takeover (ATO) Fraud: Why Financial Institutions Can No Longer Afford to Wait

HomeBlogsAccount Takeover (ATO) Fraud: Why Financial Institutions Can No Longer Afford to Wait

May 22, 2026

Key Takeaways

Account takeover (ATO) fraud is surging exponentially

Traditional defenses are facing new pressure points

AI is changing both sides of the fraud equation

The real impact of ATO goes far beyond financial losses

Numbers Do Not Lie: The ATO Surge

No single statistic captures the full scope of the account takeover (ATO) threat, but taken together, they reveal a crisis in motion.

The real story, however, is not the data itself but how your financial institution responds to it.

The Scale of the Threat

According to the State of the Fraud Report, ATO was the second leading fraud type across financial institutions in 2025, accounting for 42% of all reported cases. Among regional banks and credit unions, it ranked first.

For years, financial fraud was largely treated as a transaction issue: suspicious payments could be flagged, blocked, or reversed, with controls focused on detecting anomalies as money moved. That model is now breaking down.

Today, fraud is increasingly happening before a transaction even occurs. Instead of trying to bypass payment systems, attackers are going straight to the source, i.e., customer accounts. Once inside, every action they take looks legitimate.

It is noteworthy to observe that the attacks are not simply scaling; they are doing so exponentially and at a staggering pace.

What is Fueling the Fire: Factors Driving Acceleration

ATO fraud has quietly matured from an opportunistic crime into a systematic, industrialized threat. Four structural forces are driving the acceleration:

1. Advanced Technology and AI-based Tools

Automation allows attackers to test thousands of credential-stuffing attempts simultaneously, while generative AI has dramatically lowered the barrier to convincing impersonation. Deepfake voice and video now make social engineering attacks far more credible. 91% of decision-makers have noticed an increase in crimes committed with AI technology. What once required time and effort can now be executed quickly and at scale.

2. Fraud-as-a-Service Models

Organized fraud rings have industrialized the attack chain. Stolen credentials are also available in bulk on dark web forums. 36% of fraud events at financial institutions are attributed directly to criminal networks and fraud rings, while 31% of consumers have encountered online offers to participate in account fraud, reflecting how deeply fraud-as-a-service has embedded itself in mainstream digital culture.

3. The Human Vulnerability Gap

Technology is a part of the equation, but human behavior remains a persistent weakness. In 2025, 62% of Americans reported reusing passwords across multiple accounts. While awareness of cybersecurity risks is increasing, consistent behavioral change has not followed. Social engineering attacks exploit exactly this gap between awareness and action.

4. An Expanding Attack Surface

The continued growth of digital banking and payments is further accelerating this problem. As more customers interact through mobile apps, online platforms, and connected services, the number of potential entry points for attackers increases. Fraudsters are no longer targeting a single system; they move across ecosystems, using one compromised account as a stepping stone to another.

The True Impact of ATO: Beyond the Dollar Amount

ATO is often viewed as just another fraud category, though this framing underestimates its true impact. When an account is compromised, the consequences ripple far beyond the initial loss.

1. Customer Experience and Lifetime Value

For customers, a compromised account is deeply personal. Access to their finances is disrupted, trust is shaken, and their confidence in the institution is often permanently damaged. 50% of financial institutions report a negative impact on customer loyalty from fraud, and 44% cite brand damage, making ATO a direct threat to long-term retention.

2. Operational Friction

Fraud investigations create significant internal pressure. 47% of institutions experienced operational disruptions linked to fraud in 2025. Manual workflows strain fraud and compliance teams, driving up cost-per-case and slowing resolution times.

3. Suppressed Growth

Fraud is not just eroding revenue; it is suppressing innovation. 94% of financial institution decision-makers say fraud risk is the primary factor when deciding what new products to offer, including real-time payments and digital onboarding.

Financially, the impact is substantial too. Estimates by Aberdeen Strategy & Research suggest that credit unions risk losing up to 11% of revenue due to ATO-related issues, while banks face losses of around 7.5%. These are not marginal effects and represent meaningful threats to profitability.

What Effective ATO Defense Looks Like

The uncomfortable truth is that many existing fraud prevention systems were built for a different era. Today’s attackers do not behave like traditional fraudsters. They adapt in real time, mimic legitimate behavior, and exploit gaps across multiple channels.

Effective ATO defense requires a faster, integrated, and more adaptive infrastructure that involves:

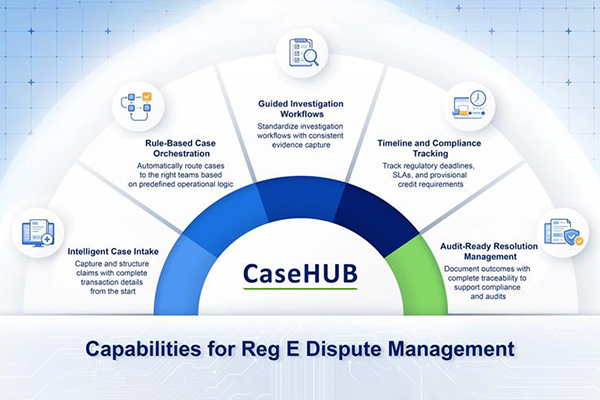

Centralized case management that brings all fraud-related activity into a single, connected environment, eliminating the siloed spreadsheets and disconnected tools that slow investigation and obscure the full picture of an attack.

AI-driven automation reduces the manual burden on fraud and compliance teams, enabling faster triage, consistent case handling, and scalable response without proportional headcount growth.

Fully auditable reporting ensures that every action taken during an investigation is logged, time-stamped, and ready for regulatory review, removing the compliance risk posed by scattered documentation.

Proactive risk mitigation shifts the posture from reactive to preventive, identifying behavioral patterns and threat signals before an account is fully compromised, rather than responding after the fact.

Configurable intelligence allows institutions to tailor their fraud identification and case management logic to their specific risk profile, customer base, and regulatory environment rather than applying generic rules that generate false positives and cause investigator fatigue.

While these capabilities are already present across most financial institutions in various forms, the real challenge lies in connecting them into a unified system that can respond quickly enough to keep pace with modern ATO attacks.

CaseHUB: Engineered for the Modern Threat

CaseHUB, an enterprise case management platform, eliminates the friction by orchestrating automation across this fragmented stack, connecting fraud signals, investigations, and compliance activities in a single environment.

It enables faster response through streamlined case workflows, reduces manual effort with AI-assisted triage, and ensures every action remains fully auditable. More importantly, it gives teams the shared context needed to move from isolated alerts to coordinated action.

In an ATO landscape defined by speed and scale, CaseHUB helps institutions build a posture that not only responds to ATO fraud but also systematically reduces the conditions that enable it to succeed.